In our recent guest expert post for the Value Reporting Foundation, we made the case that integrated reporting is a means to an end – integrated thinking.

Companies that have made the leap regularly tout the benefits of integrated thinking for meeting stakeholder expectations on ESG and supporting long-term value creation. Despite these benefits, many businesses remain reluctant to start their integrated reporting journey.

The reluctance generally stems from two misperceptions:

- An integrated report must align with the Integrated Reporting Framework in its entirety

- An integrated report involves an overhaul of existing statutory reporting, such as the SEC Form 10-K

In our Value Reporting Foundation post, we broke down the first misperception by explaining how companies can progress toward integrated thinking through selectively implementing the most impactful components of the Integrated Reporting Framework.

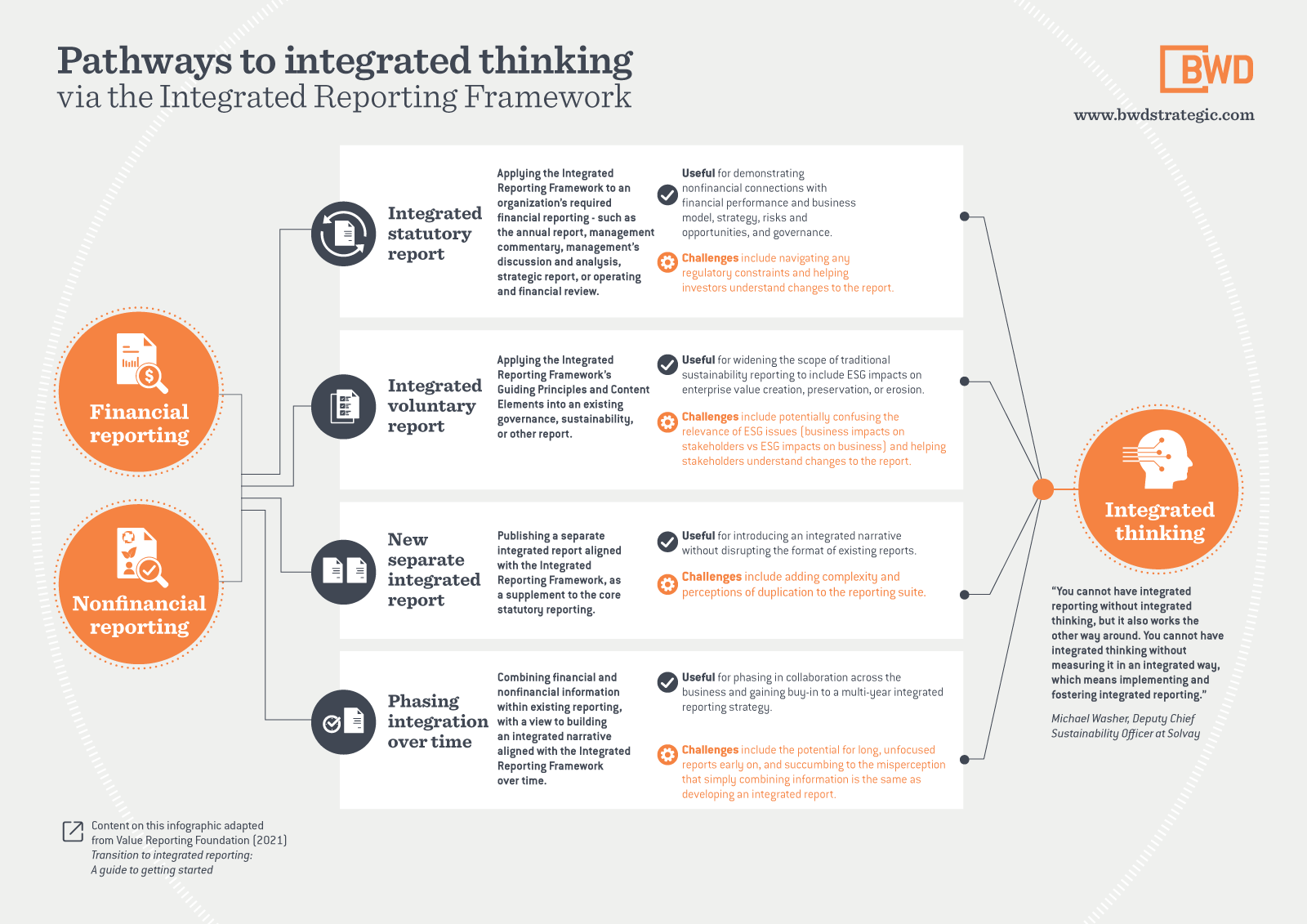

Moving to the second misperception – integrated reporting does not always mean overhauling an existing statutory report, such as the Annual Report on Form 10-K. The infographic below summarizes Value Reporting Foundation guidance on the many pathways available for implementing integrated reporting.

Download the infographic here (250kb)

Download the infographic here (250kb)Although company paths to integrated thinking will vary, there is a path for every company. If you’re ready to reap the benefits of integrated thinking, BWD can help.